Certainly! Here is a detailed, professional analysis and report in English, structured as requested, based on the theme “Crypto Rulemaking Has FinTech Rushing in, TradFi Waiting to See.” The content is organized with engaging subheadings and a logical progression.

—

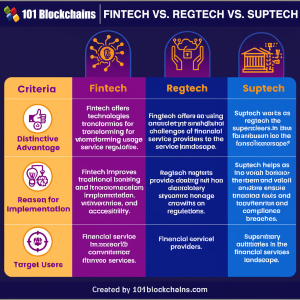

The rapid evolution of cryptocurrency regulation has set the stage for a fascinating dynamic between two major financial sectors: FinTech and traditional finance (TradFi). As new rules take shape—especially in the United States—FinTech firms are racing to adapt and capitalize on emerging opportunities, while TradFi institutions remain cautious, waiting for regulatory clarity before making significant moves. This report explores why these divergent strategies exist, what they mean for the broader financial landscape, and how both sectors are navigating an increasingly complex environment.

Introduction: A Regulatory Crossroads

Cryptocurrency markets have long operated at the edge of regulatory oversight. But as digital assets gain mainstream traction—fueled by institutional interest and technological innovation—governments worldwide are stepping up efforts to bring order to this frontier. In 2025, U.S. lawmakers are advancing bills that could fundamentally reshape how crypto is regulated: expanding jurisdiction over spot trading for agencies like the CFTC[4], tightening requirements around custody and exchange operations[4], and clarifying which tokens qualify as securities or commodities[5]. These changes have sent shockwaves through both FinTech startups eager to innovate within new frameworks and established TradFi players wary of compliance risks.

Why FinTech Is Racing Ahead

Embracing Innovation Amid Uncertainty

FinTech companies thrive on agility. Their business models often revolve around leveraging technology to disrupt traditional financial services or fill gaps left by legacy systems. With crypto rulemaking underway, many see an opportunity to establish themselves as early adopters within newly defined legal boundaries.

Regulatory Arbitrage

For some FinTechs, ambiguity itself can be advantageous. By moving quickly into areas where rules are still forming—such as tokenization platforms or decentralized finance (DeFi) protocols—they can shape industry standards before regulators catch up[2][3]. This approach carries risk but also offers first-mover benefits if their solutions align with eventual regulations.

Building Trust Through Compliance

Forward-thinking Fintechs recognize that robust compliance will be key to attracting institutional partners down the line[5]. Many are investing heavily in anti-money laundering (AML) systems, know-your-customer (KYC) procedures, smart contract audits[5], and transparent governance structures even before these become mandatory across all jurisdictions.

Why TradFi Is Taking Its Time

Risk Aversion Rooted in Legacy Systems

Traditional banks asset managers hedge funds operate under strict oversight from multiple regulators including SEC CFTC state banking authorities among others They face steep penalties if found non-compliant so any move into crypto requires careful consideration especially when classification remains unclear whether certain tokens count securities commodities other instruments altogether [4][5]

Waiting For Clarity Before Committing Capital

TradFi institutions typically require clear guidelines before allocating resources toward new asset classes Unlike nimble startups they must justify investments shareholders boards who demand evidence stable predictable environments Thus while some have dipped toes water via custody services limited trading desks most remain sidelines until legislation settles [1][4]

Operational Challenges Integrating New Technologies

Integrating blockchain-based products existing infrastructure presents technical operational hurdles Legacy systems weren’t designed handle real-time settlement tokenized assets nor do they easily accommodate pseudonymous counterparties decentralized autonomous organizations DAOs [2][5] Overcoming these barriers requires significant investment retraining staff upgrading IT architecture all which make sense only once regulatory path forward becomes apparent

The Impact Of Emerging Regulations On Both Sectors

Expanding Jurisdiction And Oversight

Recent proposals would grant CFTC authority over spot transactions involving digital commodities marking shift previous regime where only futures contracts fell under its purview [4] Meanwhile SEC continues assert jurisdiction tokens deemed securities creating potential overlap confusion between agencies especially when same asset might classified differently depending context use case issuer intent etcetera Such complexity makes it difficult firms navigate without incurring unintended violations fines enforcement actions operating bans particularly those straddling multiple jurisdictions product lines customer bases alike [4][5]

Strengthening Market Integrity And Investor Protection

New rules aim address past failures such collapse FTX Trading prohibiting proprietary trading exchanges requiring separation powers duties similar those found traditional futures markets Specifically exchanges must now keep customer funds separate qualified custodians rather than commingling them own accounts thereby reducing systemic risk counterparty exposure should another catastrophic event occur again future Additionally provisions mandating transparency governance liquidity sources treasury management help build trust among investors counterparties alike further encouraging participation from cautious institutional players once dust settles sufficiently enough signal safety stability required level comfort needed commit capital at scale beyond experimental pilots small allocations here there currently seen today across boardroom tables everywhere else too perhaps soon enough if trends continue apace directionally speaking anyway you get idea hopefully point made clearly enough already so let’s move along shall we?

Bridging The Gap Between Old And New Worlds Of Finance

As regulations evolve there growing recognition need bridge worlds old new finance effectively manage risks ensure smooth functioning global capital markets Tokenization technology cited example pathway toward de-risking shortening settlement cycles enabling near-instantaneous cross-border transfers potentially unlocking trillions dollars value currently trapped inefficient outdated processes legacy rails alone cannot support adequately anymore given demands modern economy users expectations speed convenience security privacy all rolled one seamless experience ideally speaking least theory practice may prove harder achieve reality but progress being made nonetheless thanks ongoing dialogue collaboration stakeholders policymakers technologists entrepreneurs academics others involved shaping future together collaboratively cooperatively constructively hopefully productively ultimately beneficially everyone concerned parties end day after all said done right?

Case Studies: How Firms Are Responding To Regulatory Shifts

DeFi Protocols Adapting To Compliance Demands

Decentralized finance projects historically resistant centralized control now find themselves needing demonstrate transparency accountability order attract partnerships large institutions public companies regulated asset managers Many implementing real-time disclosures treasury reserves incentive spend protocol earnings conducting regular smart contract audits providing clear audit trails decision-making authority despite inherent challenges posed by pseudonymous founders opaque token distribution strategies typical DAO-controlled environments Some even integrating third-party identity verification transaction monitoring suspicious activity reporting protocols meet AML/KYC requirements expected US counterparts thus positioning themselves favorably upcoming wave institutional adoption likely follow once dust settles sufficiently enough signal safety stability required level comfort needed commit capital scale beyond experimental pilots small allocations here there currently seen today across boardroom tables everywhere else too perhaps soon enough if trends continue apace directionally speaking anyway you get idea hopefully point made clearly already so let’s move along shall we?

Traditional Banks Testing Waters With Custody Services

Several major banks launched digital asset custody units recent years offering secure storage cryptocurrencies clients However uptake remains limited due lingering uncertainty classification treatment various coins tokens under law Until clearer guidance emerges regarding whether particular assets qualify securities commodities other instruments altogether most prefer wait sidelines rather than expose themselves unnecessary legal operational reputational risks associated premature entry untested waters especially given heightened scrutiny enforcement actions targeting non-compliant actors recent memory still fresh minds many executives directors alike hence reluctance dive headfirst just yet understandable prudent course action meantime least until more certainty achieved overall landscape evolves further favor deeper engagement longer term basis eventually maybe possibly probably depending circumstances course events unfold unpredictably sometimes always case disruptive technologies like blockchain cryptocurrencies generally speaking anyway right now though patience seems prevailing strategy among incumbents contrast newcomers who willing take calculated gambles hope reap rewards later date assuming everything goes according plan fingers crossed knock wood touch wood whatever superstition applies your culture background preference really doesn’t matter much context discussion except maybe add bit color flavor otherwise pretty straightforward analysis thus far wouldn’t you agree reader dear friend whoever reading this wherever whenever

資料來源:

[1] fintech.tv

[3] papers.ssrn.com

Powered By YOHO AI